I. Why Are So Many People Confused About dYdX?

Many people experience three typical points of confusion when they first encounter dYdX:

- Is it an "exchange" or is it a "token"?

- What exactly is a "decentralized perpetual contract," and why does it sound so complicated?

- What practical value does the DYDX token actually hold?

More realistically, a pressing question arises:

- Why do we even need dYdX when we already have mature centralized exchanges like Binance and OKX?

🧠 Core Questions This Article Solves For You

You will gain a systematic understanding of:

- The exact problem dYdX is solving

- The genuine market opportunities for decentralized derivatives

- The critical strategic transformation from v3 to v4

- The true source of value for the DYDX token (beyond mere narrative)

- The underlying price framework for the 2025–2030 period

- How to participate in DYDX safely

💡 Before diving into DeFi derivatives, it is highly recommended to establish a solid understanding of the broader market:

👉 Is it a good time to buy Bitcoin now?

This is because all exchanges and derivative sectors fundamentally rely on macro market liquidity cycles.

II. Prerequisite Knowledge: Why Do We Need Decentralized Derivatives?

2.1 Hidden Risks of Centralized Exchanges (CEXs)

Mainstream centralized platforms like Binance and OKX carry three structural risks:

- ① Asset Custody Risk: User assets are entirely controlled by the platform, leaving them exposed to potential capital misappropriation, as seen in the FTX collapse.

- ② Market Manipulation Risk: Opaque internal matching systems can result in artificial liquidations via "scam wicks" (price spikes) where liquidation prices are arbitrarily influenced.

- ③ Regulatory Risk: Shifting national policies can instantly restrict platform access, preventing users from freely moving assets across borders.

2.2 Why Did DEXs Historically Struggle with Derivatives?

Prior to recent innovations, decentralized exchanges faced massive bottlenecks:

- The automated market maker (AMM) model used by platforms like Uniswap is fundamentally unsuited for high-frequency contract trading.

- On-chain matching costs were prohibitively high.

- Network latency made it impossible to safely support high-leverage trading.

👉 The past industry consensus was clear: "Building an on-chain perpetual contract ecosystem is impossible."

That was until dYdX arrived.

2.3 How Massive is the Perpetual Contract Market?

- The Core Fact: Derivatives trading volume consistently dwarfs spot trading volume over the long term.

- Contract trading fees serve as the primary revenue source for major CEXs.

- The market penetration rate of DeFi derivatives remains incredibly low, meaning dYdX is competing in a vastly under-exploited market.

III. dYdX Project Deep Dive: Moving from Ethereum to an Independent AppChain

3.1 Project Background and Team

- Founder: Antonio Juliano, a former software engineer at Coinbase.

- Financing Lineup: Backed by top-tier capital heavyweights including a16z, Paradigm, and Polychain.

- Key Characteristic: Massive institutional backing focused on building long-term infrastructure rather than a short-term exchange project.

3.2 dYdX v3 (The Legacy Era)

- The v3 Architecture: Built on top of StarkEx (a ZK Rollup solution) featuring off-chain order matching combined with on-chain settlement.

- Advantages: Offered high performance and a highly mature trading experience.

- Disadvantages: Still contained centralized components, relied entirely on StarkEx, and relied on a revenue model heavily dependent on "subsidized growth."

3.3 dYdX v4 (The Pivotal Turning Point)

The most massive architectural shift in v4:

- 👉 Transitioned from an Ethereum application to an independent AppChain via the Cosmos SDK.

Core Architecture Highlights:

- A fully on-chain orderbook

- Decentralized network validators

- A completely sovereign dYdX Chain

Why migrate?

- The team firmly believed that without owning their own dedicated blockchain, true decentralization for derivatives could never be fully achieved.

The Game-Changer: Revenue Distribution

- 👉 100% of protocol fees are distributed directly to token stakers.

- This marks the official evolution of DYDX from a pure "governance token" into a genuine "cash-flow generating asset."

3.4 Product Capabilities

- Supports BTC / ETH perpetual contracts with leverage options up to 20x.

- Features fully transparent, on-chain orderbook execution with entirely public liquidation rules.

- Comparison with CEXs: The user interface experience may feel slightly less polished, but it offers unparalleled transparency.

💡 For a reference on infrastructure-driven utility tokens, see also:

👉 What is MASK?

IV. DYDX Tokenomics (The Core Logic of v4)

4.1 Basic Structure

- The total token supply is strictly hard-capped.

- The current circulating supply sits at a moderate level.

- Annual inflation is explicitly directed toward ecosystem growth incentives.

4.2 Allocation Structure

- Institutional Investors

- The Core Development Team

- Community Treasury

- Ecosystem Incentives

- Airdrops

4.3 Unlocking Pressures

- Key Risk Area: The period stretching from 2025 to 2027 represents the primary token unlock phase.

- Selling pressure originating from early VCs and team allocations will occur in cyclical waves.

4.4 The v4 Core Value Model (Crucial)

Under the v4 architecture, the value of DYDX is derived from three primary pillars:

- ✔ 1. Staking Dividends: Users who choose to stake their DYDX tokens receive a direct slice of the protocol's transaction fees, acting much like an exchange dividend.

- ✔ 2. Validator Yields: Delegating tokens to network validation nodes allows users to secure a portion of the baseline network rewards.

- ✔ 3. Governance Rights: Gives users the power to vote on adjustment parameters and calibrate platform fee models.

⚠️ The Fundamental Shift:

- v3 Era: DYDX = Pure Governance + Participation Incentives

- v4 Era: DYDX = Yield-Generating Asset + Governance Asset

4.5 Protocol Revenue Logic

The ultimate valuation of DYDX is bound to:

- The aggregate trading volume of perpetual contracts on the platform

- The total fee revenue generated by that volume

- Industry Benchmarks: Functions under a "chain-native brokerage model," mirroring protocols like GMX and Gains Network.

V. DYDX Price Trends & 2025–2030 Predictions

5.1 Historical Price Action Review

- Key Milestones: Early post-launch price discovery, exploding contract volumes during the peak bull market, and rally expansions driven by anticipation of the v4 migration.

- Market Correlation: Maintains a high correlation with the Ethereum ecosystem and remains heavily bound to macro BTC market cycles.

5.2 Core Price Driving Factors

Ranked in order of overall importance:

- Protocol Trading Volume (The Most Critical): This directly dictates the cash-flow yield distributed to stakers.

- DeFi Derivatives Penetration: The overarching migration of users from centralized platforms to decentralized alternatives.

- The Competitive Landscape: Pressure from competing protocols like GMX, Hyperliquid, and Vertex.

- Token Unlock Schedules: Managing the systemic supply expansion.

- Macro Bull/Bear Cycles.

💡 The ultimate upside for the derivatives sector is closely tied to the Ethereum cycle:

👉 Ethereum Price Prediction 2030.

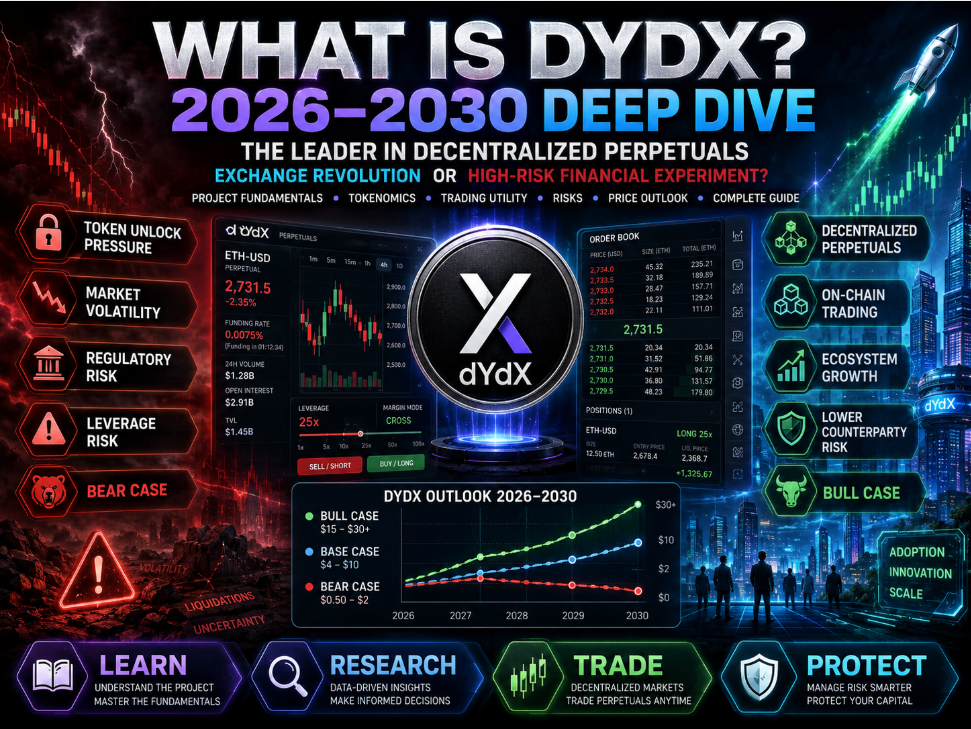

5.3 DYDX Multi-Scenario Predictions (2026–2030)

- Year 2025

- Bear Market Scenario: $0.60

- Baseline Scenario: $1.80

- Bull Market Scenario: $3.50

- Assumption: The v4 staking mechanism begins to successfully drive structural demand.

- Year 2026

- Bear Market Scenario: $0.45

- Baseline Scenario: $2.50

- Bull Market Scenario: $5.50

- Assumption: Trading volumes surge following post-BTC halving cycles.

- Year 2027

- Bear Market Scenario: $0.35

- Baseline Scenario: $2.20

- Bull Market Scenario: $5.00

- Assumption: Global regulatory frameworks regarding crypto derivatives achieve clarity.

- Year 2028

- Bear Market Scenario: $0.30

- Baseline Scenario: $3.00

- Bull Market Scenario: $7.50

- Assumption: Institutional capital actively scales into DeFi derivatives.

- Year 2030

- Bear Market Scenario: $0.20

- Baseline Scenario: $4.50

- Bull Market Scenario: $12.00

- Assumption: Decentralized derivative protocols capture a major portion of global trading market share.

⚠️ All predictions are based on model projections and do not constitute investment advice.

VI. How to Buy DYDX on HiBT

6.1 Why Choose HiBT?

- A fully compliant trading ecosystem utilizing global licensing frameworks

- Robust asset protection via institutional-grade cold wallet custody

- Deep liquidity and thin spreads for the DYDX/USDT pair

- An intuitive layout tailored for onboarding beginners

6.2 Registration Steps

- Register your account on the official HiBT platform.

- Complete the mandatory Identity Verification (KYC) requirements.

- Enable your asset and trading account configurations.

6.3 Funding Options

- Directly deposit USDT into your spot wallet.

- Utilize local fiat gateways depending on your regional availability.

- Crucial: Always double-check contract addresses and network types prior to execution.

6.4 Executing the Purchase

- Navigate to the market terminal and search for the DYDX ticker.

- Select your preferred trading pair.

- Submit a Market Order (for instant settlement) or a Limit Order (to specify your entry price).

6.5 Advanced Step: Staking DYDX

To plug into the native v4 ecosystem yield:

- Withdraw your purchased tokens to a compatible Cosmos wallet, such as Keplr Wallet.

- Delegate your tokens to a reputable network validator.

- Begin accumulating your proportional share of the protocol revenue.

- ⚠️ Note: The network unbonding period is approximately 30 days. Be sure to account for this liquidity lockup risk.

VII. Comprehensive Evaluation of DYDX Investment Risks

7.1 Technical Risks

- Security vulnerabilities inherent to the underlying Cosmos ecosystem architecture.

- Cross-chain bridging vulnerabilities during asset transfers.

- Smart contract exploit vectors.

7.2 Competitive Risks

- Market share capture by GMX v2 and other peer-to-peer liquidity models.

- The aggressive rise of high-speed orderbook alternatives like Hyperliquid.

- Centralized exchanges aggressively optimizing their fee models to retain users.

7.3 Token-Specific Risks

- Cyclical downward pressure stemming from major token unlock schedules.

- Potential volatility in the total network staking ratio, which impacts individual yield payouts.

- Governance rights can easily be diluted if a small group of entities holds a majority concentration of tokens.

7.4 Regulatory Risks

- Increased global enforcement and scrutiny on decentralized derivative trading.

- The potential for regulatory compliance mandates to impact front-end access in specific jurisdictions.

VIII. Conclusion: Who is DYDX Best Suited For?

✔ It is highly suited for:

- Investors who deeply understand the inner workings of DeFi mechanics.

- Individuals with long-term bullish conviction in the decentralized derivatives sector.

- Users looking to lock up capital to capture cash-flow staking yields.

❌ It is NOT suited for:

- Hyper-short-term momentum scalpers.

- Traders who do not understand the underlying mechanics of leverage and futures contracts.

- Investors with a very low tolerance for high-beta portfolio volatility.